Joel Davis,

Managing Director at Image Property.

What’s Next For Interest Rates?

By Joel Davis, Image Property

Interest rates exert a significant influence on property prices, so, it makes sense for homebuyers to think about where rates might be headed and how that will affect their ability to obtain and service a loan.

Among the questions savvy property purchasers ask themselves about interest rates are these three:

- What is happening with interest rates now?

- What will happen next?

- What will rates do in the medium term, say, in the next three to five years?

The good news is that our central bank rarely makes a completely unexpected move, so, if we look at the recent expert financial commentary, we may be able to form a view on what is on the horizon.

What is happening now?

Australia’s central bank is responsible for setting the nation’s monetary policy with a particular focus on jobs and inflation.

Using the cash rate to control how much money Australians have left over after paying their loan bills, the RBA is aiming to control the amount of money circulating through the economy.

When more money is left over, consumers (hopefully) spend it, adding money to the economy.

This stimulates jobs and pushes up inflation, which is a barometer of how quickly the economy is growing.

Historically, the RBA has aimed for an inflation rate of about two to three per cent, but this may be changing in the years ahead.

When unemployment is too high and inflation is too low, the RBA cuts rates, as it has been doing lately, down to the current 0.25 percent.

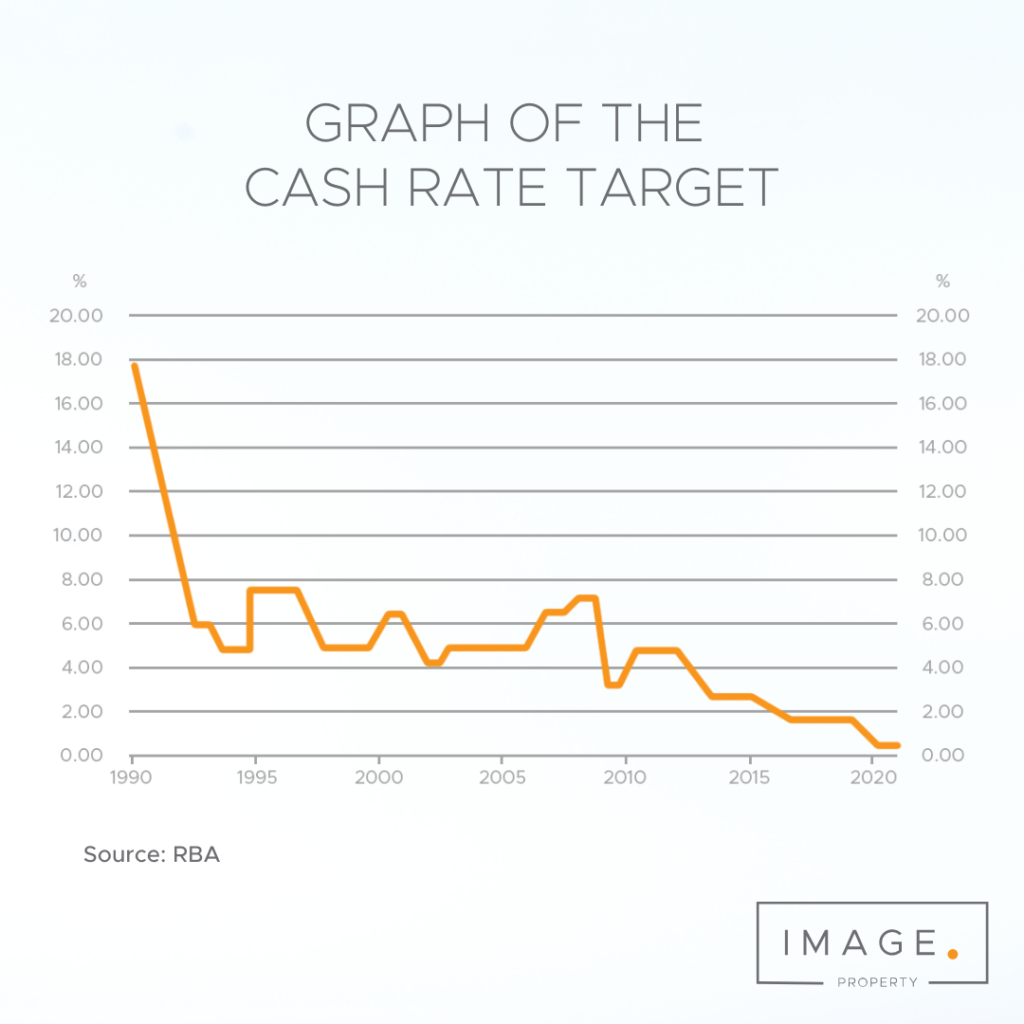

In fact, the cash rate has been trending down since 2011 as the below graph shows.

The goal is to give people more spending money, which will stimulate the economy.

What’s next?

In the minutes of its October meeting, the RBA Board acknowledged the current uncertain environment and has indicated that it would base its decisions on “actual, not forecast inflation”.

As the impact of the pandemic exerts a heavy drag on the economy, with the Melbourne shutdown exacerbating the sluggishness, the board noted the challenge of predicting household saving behaviour.

Will we spend or save? The board hopes people will spend, but the fragile jobs market has many people worried.

So, there are hints that RBA Governor Philip Lowe is preparing for an upcoming rate cut in November and experts are forecasting that cut will be 0.15 per cent to take the cash rate to just 0.1 per cent.

There is also a potential for quantitative easing via large scale bond buy-ups.

What’s on the horizon?

Given unemployment amid the COVID pandemic is tipped to remain elevated for some time to come, and inflation has been subdued for a few years, it is unlikely that the RBA will move to a raising cycle anytime soon.

An interest rate rise would require low unemployment, which is currently sitting at around 6.9 per cent, as well as higher inflation.

So, it is safe to say that a low-rate environment will continue over the next three to five years.

The RBA takes unemployment and inflation figures as key indicators about the state of the economy when making a decision about rates.

Rates have been trending down since November 2011, pushed down by a soft jobs market and low inflation following the GFC.

Given that the pandemic is likely to be an ongoing factor for some time to come, it’s fair to say that a low interest rate environment will be the new normal for a long while yet.